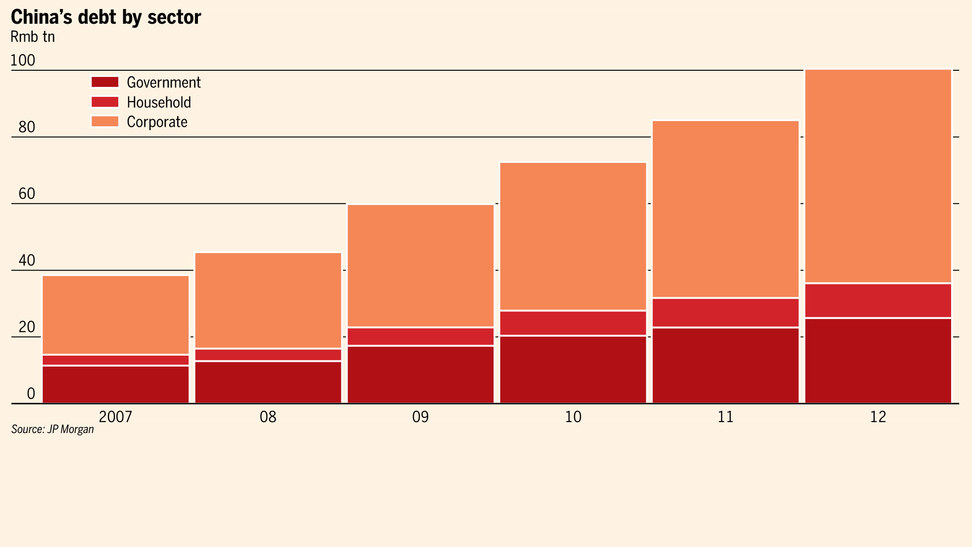

Paul Davies at FT Alphaville argues that the $3.4tn in foreign reserves that China holds cannot be used to address with their problems of bad debt. The article follows a series of reports by the FT on the increasing and unsustainable amount of debt that we see in China these days. As an example, here is a chart from one of those earlier reports.

From the chart we see increasing levels of debt by all sectors of the Chinese economy. So China looks like the US now... or not. The data on debt is just a partial view on the balance sheet and the potential instability of a financial system. It measures liabilities, it does not look at assets.

What happens if we look at the value of assets in the Chinese economy? They are increasing at a faster rate than debt. How do we know that? Because we know that China has been running a current account surplus, a sign that income exceeded spending and therefore the country was a net saver.

The accumulation of current account balances does not exactly correspond to the net foreign wealth of a country because there can be valuation changes over time. I might save $100 today and buy shares in the stock market or a foreign government bond. My wealth tomorrow might change by more or less than $100 depending on how the prices of those assets change. Pierre-Olivier Gourinchas and Helene Rey have produced some neat analysis on how these two magnitudes differ for many countries, here is their chart for China.

The red line corresponds to the accumulation of current account surpluses (expressed as $ of GDP), this is the flow of saving. The blue line is the actual value of their "net foreign wealth". In the case of China the blue line is below the red one which means that China has suffered valuation losses in their external balance sheet; the value of their assets has appreciated less than the value of its liabilities (this could be partially due to the fact that their assets tend to be riskless while their liabilities tend to be of the form of FDI).

Where do foreign reserves enter into the picture? The accumulation of foreign reserves comes from two sources: the funds generated from current account surpluses and the (net) investment flows into China. For example, when a multinational invests in China (FDI), that flow, if unmatched by any other flow, leads to an accumulation of foreign reserves. As Paul Davies points out in his article, those reserves cannot be simply considered wealth of China because FDI represents a liability. Correct. The right number is the one where all assets and liabilities are taken into account, which is the blue line in the Chart above, the net foreign asset position which stands just below 30% of Chinese GDP (about $2tn). This number is indeed lower than the total amount of foreign reserves that China holds ($3.4tn).

So China is a country of savers and borrowers, like any other. In aggregate, the country saves as reflected by a current account surplus. Its nets foreign asset position is about $2tn, a true measure of the health of the external balance sheet of China. The amount of foreign reserves is not the right measure as it exaggerates the foreign wealth position. And for the same reason, the first chart with the debt numbers provides a too pessimistic view of the Chinese financial health. Both of these figures are just partial views on the Chinese balance sheet.

Given that net foreign wealth in China is positive and increasing, does it mean that there should be no concerns about the increasing debt in some sectors of the economy? No. There are two things to worry about. First, the fact that some (individuals, corporations, government) are accumulating debt could put them at risk even if others in the economy are saving. Financial fragility is not only about the average position it is also about the individual saving/borrowing positions. Second, some of the borrowing goes to fund purchases of domestic assets that might have an inflated value. So even if today when we aggregate assets and liabilities the balance sheet looks healthy, we could have asset values collapsing and sending the net wealth of individuals to a situation that leads to defaults, need for deleveraging and a crisis (as we have seen in many advanced economies).

Antonio Fatás